Tata Motors Q3 Results: Reports Profit After Seven Quarters Of Losses

Tata Motors Ltd announced its results for quarter ending December 31, 2022. The results represent the details on consolidated segment level.

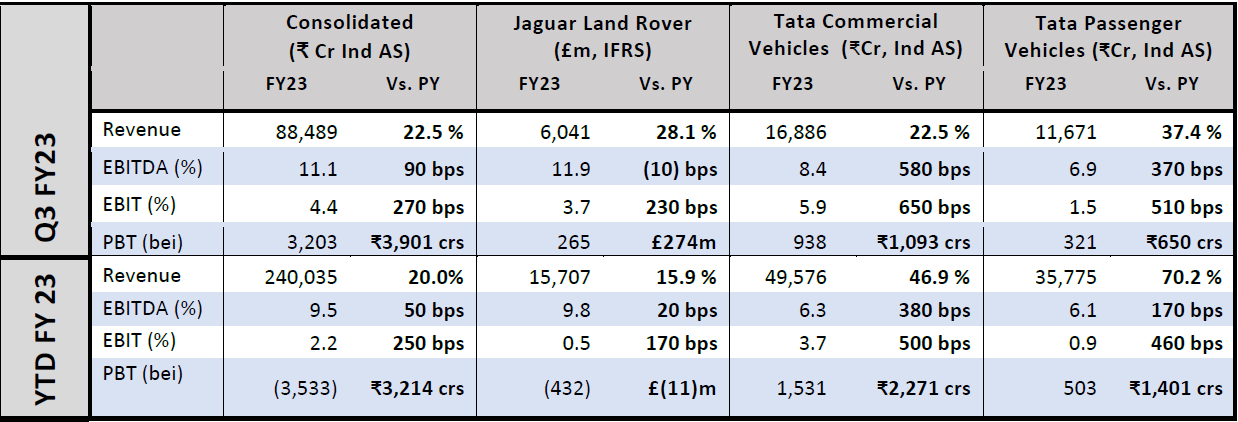

Jaguar Land Rover (JLR): JLR delivered on its plans and achieved positive free cash flow and profitability in the quarter as supplies improved. Revenues were £6.0 billion, up 28% vs. Q3 FY22 and up 15% sequentially reflecting better supplies, strong model mix and pricing. Profit before tax in the quarter was £265 million, up from a loss of £(9) million a year ago with a positive EBIT margin of 3.7%, up from 1.4% in Q3 FY22. The higher profitability reflects increased wholesale volumes with favourable mix, pricing and foreign exchange offset partially by higher inflation and supplier claims largely related to constrained volumes. Free cash flow was £490 million in Q3 FY22.

Tata Commercial Vehicles (Tata CV): Tata CV revenues in Q3 FY23 were up 22.5% vs. Q3 FY22 at ₹ 16.9KCr. Q3 FY23 EBITDA margins were 8.4% (+580 bps yoy) and EBIT margins were at 5.9% (+ 650 bps y-o-y) led by better mix, higher realisations, cost savings and softened commodity prices. The business was PBT (bei) positive at ₹ 0.9K Cr as compared to loss of ₹ 0.2K Cr in Q3 FY22.

Tata Passenger Vehicles (Tata PV): Tata PV revenues were up 37% vs Q3 FY22 at ₹ 11.7K Cr reflecting higher volumes and realizations. EBITDA margins were 6.9% (+370 bps yoy) and EBIT margins were at 1.5% (+510 bps) yoy driven by improved volumes and mix, higher realizations, softening commodities and certain one offs. The business was PBT (bei) positive at ₹ 0.3K Cr as compared to loss of ₹ 0.3K Cr in Q3 FY22.

Outlook: “We remain cautiously optimistic on the demand situation despite global uncertainties. We will remain vigilant on demand and our continued focus on profitable growth, improving semiconductor supplies and stable commodity prices will aid revenue growth, margin improvement and positive cash delivery in Q4 FY23.”